What is Segregation of Duties in 2026?

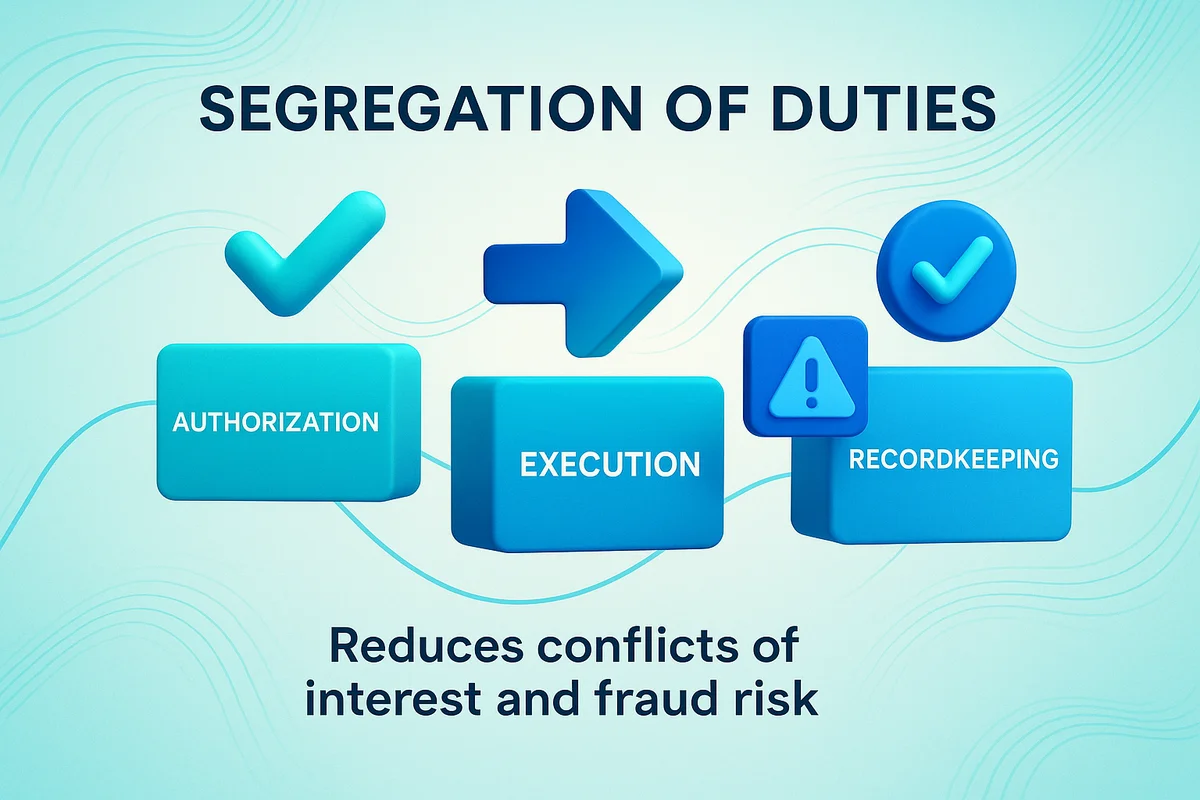

Segregation of duties reduces conflicts of interest and fraud risk by enforcing independent approvals, audit trails, and checks

Ask about this article

Opens Claude in a new tab to answer, using this article as the source.

Segregation of duties keeps critical tasks separated to limit risks and reduce operational errors. By splitting responsibilities you make it harder for mistakes and fraud to hide, and you build clearer evidence trails for later review.

Separating approval and execution prevents a single person from controlling high-risk transactions across systems. It forces independent approvals, creates audit trails, and makes every step traceable for auditors and investigators chasing inconsistencies or fraud.

Within IT and compliance, SoD overlaps with identity and access management, change control, and transactional systems. Teams often juggle competing priorities, which complicates implementing strict role separation. That tension means organizations rely on risk-based choices and compensating checks when ideal separation isn’t practical.

Effective SoD enforces role separation and least-privilege access across users, roles, and transactions. Controls can be preventive or detective, operating at different layers to stop risky actions or flag them for review when they occur. When full separation isn’t feasible, compensating controls fill gaps.

This article breaks down SoD, why separating duties stops conflicts and fraud, and where violations show up. It also examines how automation and regular audits help enforce controls and keep segregation effective over time.

Table of Contents

- What is segregation of duties (SoD)?

- How does SoD prevent fraud and conflicts of interest?

- Where do SoD violations commonly occur?

- How do automation and audits enforce SoD?

What is segregation of duties (SoD)?

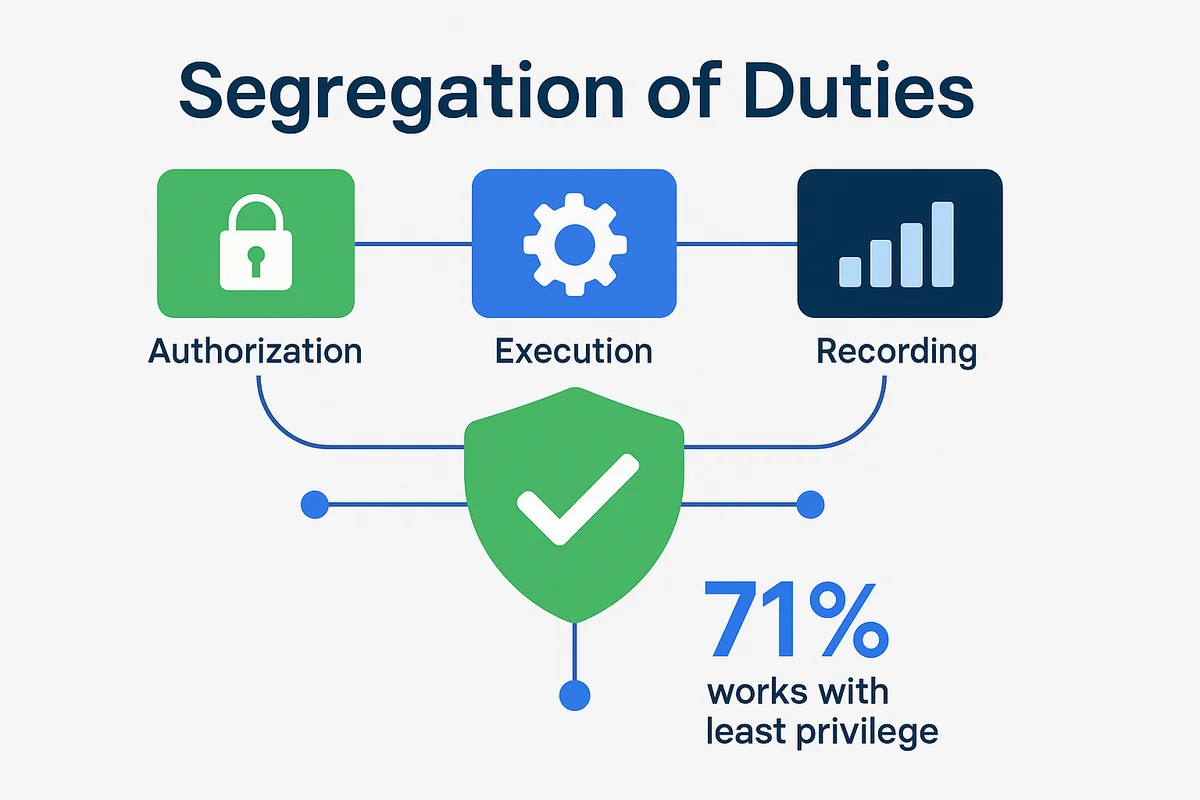

Segregation of duties prevents a single person from completing a critical IT transaction from start to finish alone.

SoD splits authorization, execution, and recording among different roles to create checks and balances across systems and people. The principle of least privilege works with SoD, limiting users to only the access necessary for their role and preventing extra permissions that bypass controls. Good role design maps tasks to distinct functions so approval flows, operational steps, and ledger entries don’t overlap in a single user account.

Organizations apply SoD across technical and business processes where a single mistake or abuse could cause big harm.

Common IT and compliance domains where SoD matters include these operational and technical areas that often intersect with finance:

- Identity and access management (provisioning, role assignment, and privileged accounts)

- Change control systems (code promotion, configuration changes, and release approvals)

- Transactional platforms (ERP entries, procurement workflows, and invoice processing that drive payments)

These areas often combine system privileges with financial or operational impact, so clear role boundaries are essential. Standards like COSO and the Sarbanes-Oxley Act expect controls that stop a single person from managing end-to-end financial processes.

Preventive and detective approaches play different parts in a complete SoD strategy. Preventive controls aim to stop risky role combinations by design, while detective controls flag when separation has failed or exceptions arise and prompt review. Even when strict separation isn’t practical, compensating controls offer temporary safeguards such as time-limited approvals and independent reconciliations that lower risk until a permanent fix is implemented.

Designing SoD combines technical setup with organizational processes and governance. Over time, role drift and business change will create gaps, so SoD should be maintained as an ongoing discipline rather than a one-time project.

How does SoD prevent fraud and conflicts of interest?

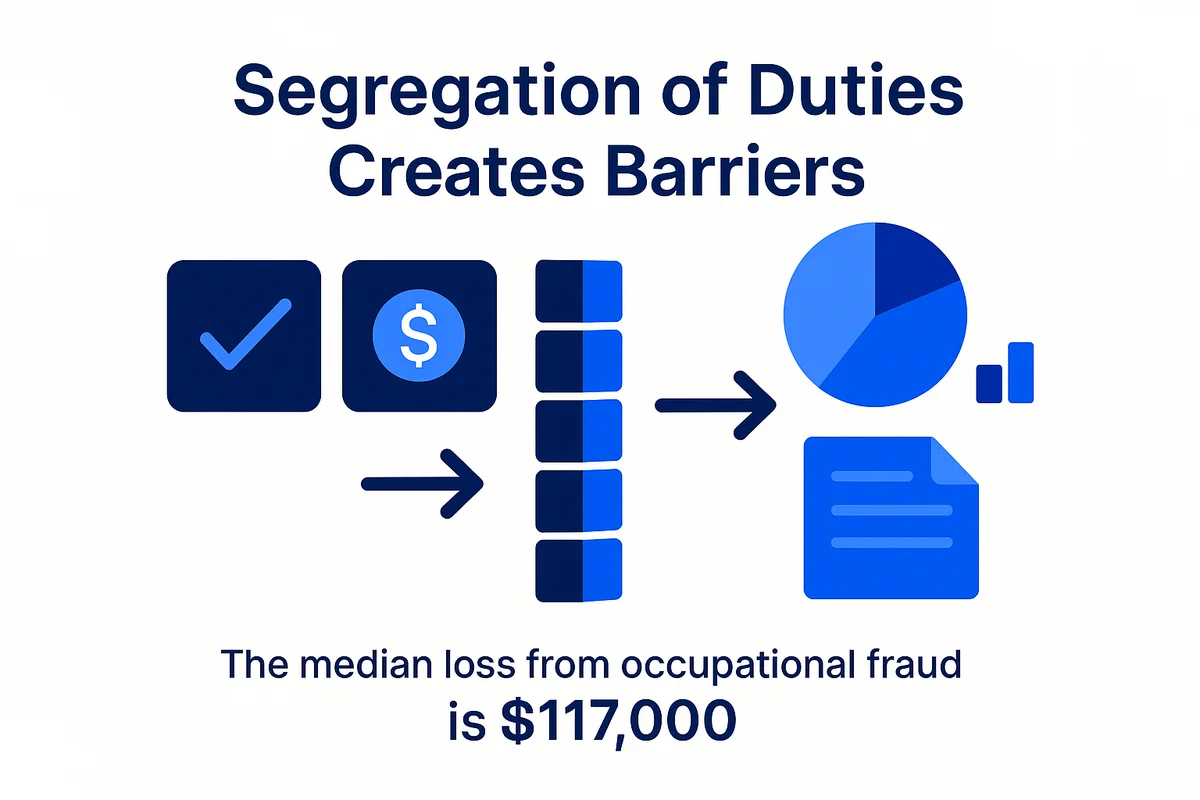

Segregation of duties creates barriers that force checks before anything sensitive can happen. Those barriers turn single points of control into deliberate, observable steps so problems surface sooner and are easier to fix.

By splitting approval, execution, and recording across people, organizations turn single-user opportunities into multi-step processes that reveal intent and errors early. When a high-risk action needs two approvals or a separate reviewer, accidental mistakes are far less likely to become material losses, and deliberate misuse becomes harder to conceal because more people touch the record and more evidence is produced.

Independent checkpoints also make activity auditable and explainable to regulators and investigators. Audit trails, immutable logs, and clear approval chains mean auditors can follow a transaction from request to settlement without guessing who did what or when. The Association of Certified Fraud Examiners reports the median loss from occupational fraud at about $125,000, underscoring how costly weak controls can be; stronger SoD shortens time to detection and increases the chance of recovery. Even so, SoD is not only about catching fraud after the fact. It embeds prevention into daily work, reducing findings in controls testing under SOX and other frameworks, and helping teams show evidence during audits.

Separation raises the bar for collusion and hidden manipulation by adding more moving parts. Those extra steps create friction that most fraud schemes can’t survive, and the added records and timing constraints expose attempts at concealment.

These practical mechanisms put segregation into daily operations and reduce the overall risk of fraud and error:

- Dual-authorization requirements for high-value transactions that require two independent approvers before funds move

- Mandatory independent reconciliation plus verification steps before any journal posting is finalized and recorded

- Distinct and documented roles for provisioning, approving, and auditing access that separate duties across teams

- Enforced rule sets and technical controls that automatically block conflicting role combinations and prevent unauthorized assignments

These mechanisms also feed monitoring and analytics tools, improving signal-to-noise for investigators. When exceptions or unusual timing patterns appear, continuous checks and cross-verified records make it faster to investigate, contain, and remediate issues. The combined effect is a smaller attack surface, clearer evidence trails for auditors, and fewer opportunities for conflicts of interest to produce financial harm.

Where do SoD violations commonly occur?

SoD violations commonly appear where users have overlapping access to money, vendors, or systems. That overlap creates opportunities for errors and intentional misuse that can be hard to spot without focused testing.

Common, recurring violations reveal where auditors and control owners should test first.

- A user who can both create vendors and approve supplier invoices, letting fake vendors get paid.

- Requesters who approve their own purchase orders and then receive the goods, bypassing receiving checks and sidestepping independent verification.

- Payroll operators who can add employees and authorize payments, enabling ghost-employee schemes and inflating payroll without separate oversight.

- Developers who push code to production and can alter or delete audit logs, obscuring mistakes or tampering.

- Administrators who grant privileged access and also perform access reviews, defeating attestations and masking who really has critical privileges.

Detecting these violations means watching for unusual combinations and transaction patterns that point to control gaps. Look for the same user IDs assigned to conflicting roles across ERP, procurement, and identity systems, repeated vendor changes without independent approvals, approvals posted at odd hours, or missing receiving confirmations. Historic cases like Enron and WorldCom showed how weak role separation and executive overrides allowed financial reporting errors and manipulation to persist undetected. ACFE data shows median fraud losses often exceed six figures and schemes often last more than a year before discovery, so catching problems early reduces risk.

When internal auditors plan testing, prioritize collusion-prone paths and single points of failure that link authorization to settlement or recording. Sample supplier lifecycles end to end, trace high-value transactions across systems, and match provisioning logs against access review records to find gaps. Pay special attention to cross-system identity mismatches and timing anomalies between creation and approval events, since those patterns often reveal covert workarounds. Focusing audits this way makes it practical to spot where segregation of duties breaks down and where controls need reinforcing.

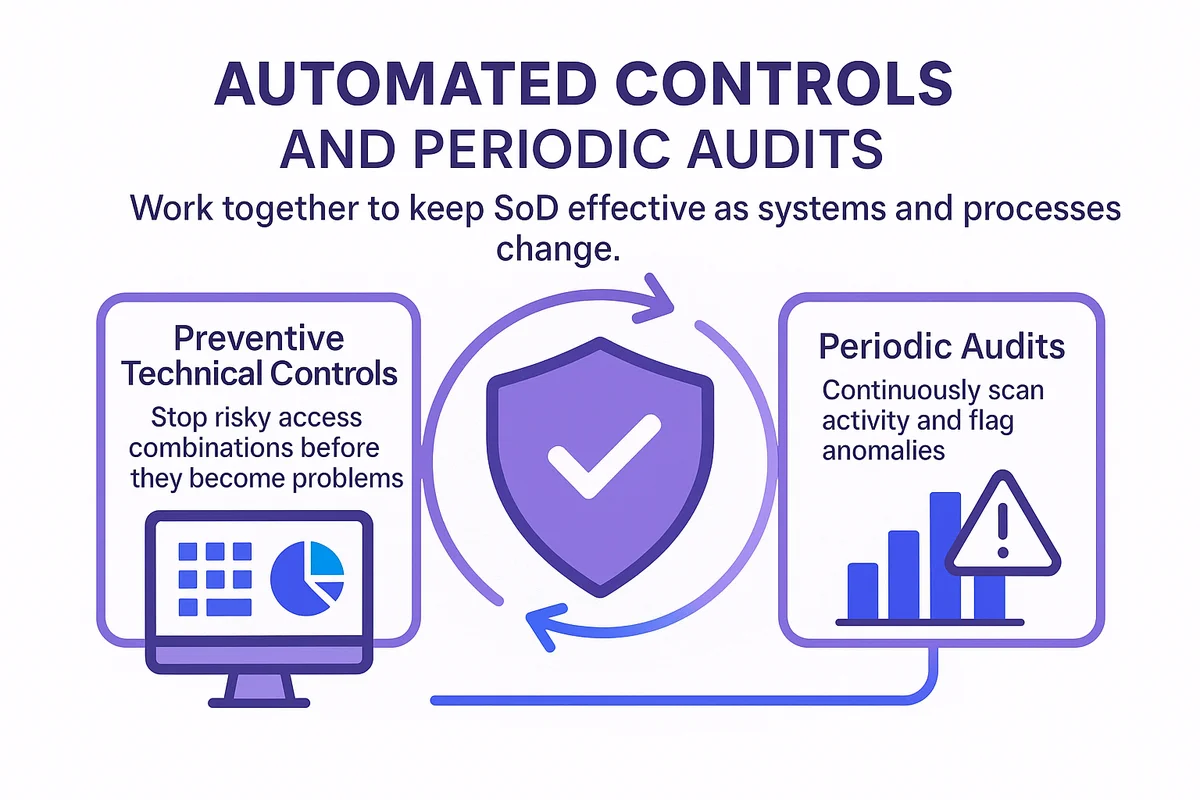

How do automation and audits enforce SoD?

Automated controls and periodic audits work together to keep SoD effective as systems and processes change.

Preventive technical controls stop risky access combinations before they become problems, using role-based access control, attribute checks, and enforced approval workflows. Many ERP platforms, including SAP and Oracle, ship with prebuilt SoD rule libraries that speed deployment and reduce guesswork. Clear rules let provisioning systems block any assignment that would create a conflict.

Detective controls continuously scan activity and flag anomalies so teams can respond faster. Typical detective tools include:

- Continuous monitoring engines that spot role conflicts and risky transactions

- Dashboards that organize violations by risk, owner, and business unit

- Alert rules that route high-risk items to security or compliance teams

Dashboards and alerts tie detections to owners and workflows, so teams can act quickly and auditors get clear evidence.

Corrective processes and governance close the loop when controls flag exceptions or changes are needed. Automated remediation can revoke access, open tickets, and record what changed while exception workflows document compensating controls and approvals. Identity platforms like SailPoint and Workday simplify certification campaigns, attestation evidence, and exportable logs for audit review. Run access certifications monthly for high-risk roles and quarterly for medium-risk areas to prevent stale privileges from accumulating.

Combine automation with independent audits to keep SoD resilient as your business evolves. Auditors should review rule definitions, exception trends, remediation times, and test sampled transactions to catch control drift early. Track a small set of metrics, such as total violations, average remediation time, percent of exceptions older than 30 days, and trend direction, and use those signals to tune rules, prioritize fixes, and show regulators clear evidence of control effectiveness.

Conclusion

This article explains how segregation of duties applies in IT and compliance settings. It shows why separating authorization, execution and recordkeeping creates checkpoints, exposes violations in finance and access controls, and points to where automation and audit steps help. Such an audit trail matters. We also cover how to combine automation with regular audits so teams keep controls working.

Segregation of duties cuts conflicts of interest and lowers fraud risk across systems and teams. It enforces independent approvals, preserves clear audit trails, and requires more than one person to perform key steps so no single user controls an entire process. That approach reduces chances of abuse and simplifies investigations when issues appear.

Audit your company’s SaaS usage today

If you’re interested in learning more about SaaS Management, let us know. Torii’s SaaS Management Platform can help you:

- Find hidden apps: Use AI to scan your entire company for unauthorized apps. Happens in real-time and is constantly running in the background.

- Cut costs: Save money by removing unused licenses and duplicate tools.

- Implement IT automation: Automate your IT tasks to save time and reduce errors - like offboarding and onboarding automation.

- Get contract renewal alerts: Ensure you don’t miss important contract renewals.

Torii is the industry’s first all-in-one SaaS Management Platform, providing a single source of truth across Finance, IT, and Security.

Learn more by visiting Torii.

Frequently Asked Questions

Segregation of duties (SoD) prevents a single person from completing a critical transaction end-to-end by splitting authorization, execution, and recording among distinct roles. It pairs with least-privilege access and clear role design to create checks, audit trails, and reduced error or fraud risk.

By requiring independent approvals and separating execution from recording, SoD creates multi-step workflows that expose intent and errors early. Multiple handlers produce audit trails and timing constraints, making collusion harder to hide and speeding detection and recovery when fraud or mistakes occur.

Common violations appear where one user controls vendor creation, invoice approval, payroll edits, or privileged system changes. Overlapping access across ERP, procurement, identity, and change-control systems creates single points of failure that auditors should prioritize for testing and remediation.

Preventive controls block risky role combinations via RBAC, enforced workflows, and provisioning rules. Detective controls continuously scan logs, flag anomalies, and surface violations to dashboards and alerts. Together they stop many issues and ensure exceptions are routed for timely review and remediation.

Automation enforces policies through provisioning, rule libraries, continuous monitoring, and automated remediation. Independent audits review rules, exception trends, and sampled transactions. Combined, they maintain control effectiveness, reduce stale privileges, and provide exportable evidence for regulators and internal stakeholders.

When full role separation isn't practical, compensating controls limit risk temporarily: time-limited approvals, dual signatures, independent reconciliations, enhanced monitoring, and documented exceptions with management sign-off. These measures reduce exposure until permanent role redesigns or automation can enforce proper separation.